Finance

sourcingjournal.com

sourcingjournal.com

[Archived version](http://web.archive.org/web/20241008212700/https://sourcingjournal.com/topics/business-news/shein-scrutiny-london-imports-xinjiang-ipo-forced-labor-530182/) Human rights concerns continue to dog China's fast fashion retailer Shein‘s initial public offering (IPO) in the UK If Liam Byrne—a British Labour Party politician who leads parliament’s business and trade committee—gets his way, Shein might need to redirect its planned IPO float to Hong Kong or its home base in Singapore. He is calling for the U.K. government to ban imports made in the Xinjiang region in China, according to the Financial Times. That kind of legislative change will result in greater intensive scrutiny in the supply chain, and ultimately on producers such as Shein over alleged use of forced labor. Xinjiang is the Chinese region with links to the exploitation of Uyghurs and other Muslim ethnic groups via forced labor. The evidence of crimes against humanity are widely documented. [...] Even those connected to the fast-fashion firm end up getting pulled into Shein controversies. Last month, Italy launched a greenwashing probe into Shein. The Italian antitrust watchdog is probing Infinite Styles Services Co., a Dublin-based operation that manages Shein’s online presence. The probe’s focus is over the possibility of misleading sustainability claims connected with Shein’s clothing. Last month, Italy launched a greenwashing probe into Shein. The Italian antitrust watchdog is probing Infinite Styles Services Co., a Dublin-based operation that manages Shein’s online presence. The probe’s focus is over the possibility of misleading sustainability claims connected with Shein’s clothing. And in August, David Schwimmer, the leader of the London Stock Exchange Group, found himself pushing back on allegations that the Exchange had lowered its standards to court Shein so it could switch course from the U.S. to the U.K. for its flotation. [...] Shein initially planned to file its IPO in the U.S., but drew scrutiny from Washington lawmakers, who urged the Securities and Exchange Commission to block the firm due to concerns over ties to the Chinese government and alleged use of forced labor in its supply chain. [...] [Given the scrutiny in the UK], the most likely scenario could be a listing on the Hong Kong Stock Exchange. [...] But how a Hong Kong listing would fare also remains a big question mark. Hong Kong isn’t exactly the go-to choice for companies aiming to go public. Exchanges elsewhere, such as the U.S. or London, are seen as more active, and therefore get to attract more investors.

theins.ru

theins.ru

[Archived link](https://web.archive.org/web/20241003223325mp_/https://theins.ru/en/opinion/valery-kizilov/275004) On Sept. 13, the Central Bank of Russia raised its key interest rate to 19% and warned of further hikes to come. The Central Bank claims the move was necessary to combat inflation, which it attributes to an alleged excessive rise in domestic demand. However, there is an alternative viewpoint. According to economist Valery Kizilov, it was the Central Bank itself that fueled inflation by unjustifiably expanding the monetary base for years while simultaneously encouraging a credit boom. Russia has grown accustomed to living with an inflation rate of close to 10%, negligible real growth, and interest rates on loans exceeding 25% per year. Breaking away from this course is difficult, writes Kizilov, and those caught up in the euphoria tend to ignore the risks and disregard the future.

**The People's Bank of China (PBoC) lowered the reserve requirement ratio (RRR) for banks by 50bps, the second reduction this year aimed at bolstering a stuttering economy. The change, which takes effect today, Sept. 27, was signaled earlier in the week by Governor Pan Gongsheng, bringing the weighted average RRR to 6.6%.** This move will free up about CNY 1 trillion in new lending, with the central bank leaving room for another cut this year. Additionally, the PBoC trimmed the 7-day reverse repo rate by 20bps to 1.5%. This rate is used to determine the nation's key lending rates. It also stated interest rates for 14-day reverse repos, as well as temporary repos and reverse repos, will continue to be adjusted in line with changes to the 7-day reverse repo rate. China has ramped up the rollout of policy initiatives this week, with its top decision-making body, the Politburo, pledging to introduce further fiscal and monetary support measures to prevent further deterioration of the econom

www.icis.com

www.icis.com

cross-posted from: https://feddit.org/post/3202701 > China’s problem is essentially that it has too much debt. > > The main role of debt is to bring forward demand from the future. [...] China’s stimulus has kept on increasing since 2008, until it peaked with the end of the pandemic. > > Now China risks entering a classic ‘debt trap’ where new loans are taken out to repay existing debt – not to create new demand. In other words, the debt is no longer being used to generate growth. In turn, this risks generating a downward spiral. > > [...] > > The underlying problem, of course, is China’s massive housing bubble. It was probably the largest ever seen. And it has been bursting for some time, with home sales slumping, as the Bloomberg chart shows. > > [...] > > China needs to urgently boost [domestic] consumption and downsize manufacturing. > > [...] > > - Housing is currently unaffordable for most people > - The real estate market is an outsize risk for the economy – it is 29% of GDP, and 70% of China’s urban wealth > - Given China’s ageing population, it seems likely [that housing sales] volume could drop at least another 20% before the market bottoms > - That will mean China will need to import a lot less oil, metals, plastics and everything else connected to the bubble. >

cross-posted from: https://feddit.org/post/2778752 > Demand for new Estonian government bonds totalled EUR 821mn, which was four times more than the EUR 200mn offered, the Ministry of Finance announced, ERR reports. > > Altogether 28 professional investors and 7,304 retail investors participated in the public bond offering. Retail investors subscribed to bonds worth EUR 29mn and will receive 100% of the amount subscribed to. Estonian professional investors will receive 26% and international investors 13% on average. > > Trading in Estonian bonds will begin on the Nasdaq Tallinn stock exchange on 17 September 2024. The bonds will mature on 16 September 2026, yielding a fixed annual interest rate of 3.3%.

China's shadow bank Zhongzhi exploited risky and potentially illegal practices before its collapse last year - Zhongzhi units engaged in potentially illegal practices before Chinese shadow bank's collapse, records show - Practices involved guaranteeing returns; using new investor funds to pay returns on existing wealth management products - Chinese regulators had prohibited capital pool business and guaranteeing of returns to prevent financial instability - Zhongzhi and relevant units did not respond to Reuters queries about such practices Zhongzhi Enterprise Group, a former leader of China's shadow banking sector that declared insolvency last year, used aggressive and potentially illegal sales practices to sustain its operations as it lurched toward collapse, according to new records. China's years-long property boom had propelled Beijing-headquartered Zhongzhi to the top of the country's $18 trillion asset-management industry and made it a key player in a shadow banking sector the size of the French economy. Asset managers such as Zhongzhi sell wealth-management products to investors. The proceeds are then channeled by licensed trust firms like its Zhongrong unit to developers and other companies that cannot tap bank funding directly because of poor creditworthiness or other reasons. Previously unreported details show that about a year before its financial troubles burst into the open, Zhongzhi units were paying returns to existing investors in wealth-management products by using funds from new investors, and promising individual investors lucrative returns that belied the group's exposure to a deepening property crisis. China's trust firms are known as shadow banks because they operate outside many of the rules that govern commercial lenders. But China's top banking regulator in 2018 specified that financial institutions including shadow banks and asset managers should not set up capital pools, to prevent them from using money from new sales to cover returns on existing wealth-management products, nor should they guarantee returns on wealth-management products.

cross-posted from: https://feddit.org/post/2595239 > Major Russian banks have called on the central bank to take action to counter a yuan liquidity deficit, which has led to the rouble tumbling to its lowest level since April against the Chinese currency and driven yuan swap rates into triple digits. > > The rouble fell by almost 5% against the yuan on Sept. 4 on the Moscow Stock Exchange (MOEX) after the finance ministry's plans for forex interventions implied that the central bank's daily yuan sales would plunge in the coming month to the equivalent of $200 million. > > The central bank had been selling $7.3 billion worth of yuan per day during the past month. The plunge coincided with oil giant Rosneft's 15 billion yuan bond placement, which also sapped liquidity from the market. > > "We cannot lend in yuan because we have nothing to cover our foreign currency positions with," said Sberbank CEO German Gref, stressing that the central bank needed to participate more actively in the market. > The yuan has become the most traded foreign currency on MOEX after Western sanctions halted exchange trade in dollars and euros, with many banks developing yuan-denominated products for their clients. > Yuan liquidity is mainly provided by the central bank through daily sales and one-day yuan swaps, as well as through currency sales by exporting companies. > > Chinese banks in Russia, meanwhile, are avoiding currency trading for fear of secondary Western sanctions.

www.bnnbloomberg.ca

www.bnnbloomberg.ca

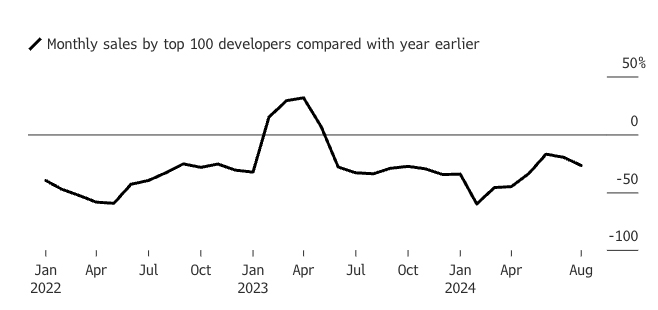

Vanke had a short-term refinancing gap of about 12 billion yuan ($1.69 billion) at the end of June due to a spike in long-term debt within a year, according to Bloomberg calculations based on company data. That’s the first time Vanke’s cash balance has failed to cover interest-bearing debt maturing in less than a year since at least 2014. As a bellwether for China’s real estate crisis, Vanke’s debt troubles underscore how even the highest quality developers have been ensnared by the unprecedented property downturn. While it’s managed to avoid a default so far, Vanke’s connections with the nation’s financial and government-backed entities means its distress could eclipse the turmoil wreaked by defaults at rivals China Evergrande Group and Country Garden Holdings Co. [...] China’s housing rescue package in May is losing steam as home sales slump deepened in August and prices are expected to plummet further. Concerns intensified in recent weeks after a string of disappointing earnings reports from consumer companies and a cut to China’s growth forecast by UBS Group AG. The downgrade reflects an emerging consensus that the country may miss its growth target of around 5% in 2024. [...] Vanke’s earnings report on Friday showed how much the extended housing slump is taking its toll on China’s fourth-biggest developer by sales. The company posted a net loss of 9.85 billion yuan for the six months ended June 30, its first semi-annual loss since at least 2003. That’s higher than the upper range flagged by the firm in July, and compares with an annual profit of 12.2 billion yuan last year. Vanke’s loss signals its finances took a sharp hit in the second quarter, considering it lost just 362 million yuan in the first three months. The slowdown in China’s market has deepened since then, as sales and prices continue to fall. Local governments are dialing back intervention over pricing of new residential projects, driving developers to offer deep discounts to lure buyers. [...]

dailynewshungary.com

dailynewshungary.com

cross-posted from: https://feddit.org/post/2261331 > [Archived link](https://web.archive.org/web/20240825021930/https://dailynewshungary.com/hungary-debt-china-grow/) > > Hungarian media outlet 444 has compiled a list of the outstanding debts of the state of Hungary, primarily using data from the Public Debt Management Centre (ÁKK). Their findings show that in just three years, the Hungarian government has accumulated considerable debt to China. By the end of the second quarter of this year, Hungary owed HUF 71.79 billion (EUR 182 million) to the Asian Infrastructure Investment Bank, a debt first incurred in the last quarter of 2022. > > Earlier, in the second quarter of 2022, Hungary secured a loan for the construction of the Budapest-Belgrade railway line. So far, they have drawn down HUF 341.6 billion (EUR 866 million) for this project. The total investment for the railway amounts to HUF 750 billion (EUR 1.9 billion), of which 85% is being financed by loans and 15% by co-financing. Additionally, in the spring of this year, Hungary requested a loan of EUR 1 billion in complete secrecy by the end of the second quarter, according to the ÁKK’s accounts. > > On top of these loans, Hungary also has CNY 3 billion worth of foreign currency bonds due for repayment to Chinese investors this year and next, which equates to around EUR 380 million at the current exchange rates. In total, 444 estimates Hungary’s debt to China now exceeds HUF 1,000 billion (EUR 2.536 billion), although they caution it could be even higher.

If anyone here is interested in a more technical interview, here are two socialists with doctorates in economics talk about why after two hundred years of talking about fixing the housing market haven’t gotten anywhere.

cross-posted from: https://feddit.org/post/1975503 > [Archived link](https://web.archive.org/web/20240815104828/https://www.cfr.org/blog/chinas-imaginary-trade-data) > > The most important part of the [International Monetary Fund] IMF’s latest assessment of China is—alas—the appendix on China’s new methodology for calculating China’s trade balance. > > It at least explains why China’s balance of payments trade surplus diverges from China’s customs trade surplus, and why the gap started to explode around 2022 [...] China’s data doesn't agree with itself. One measure of the goods deficit is a lot bigger than another measure of the goods surplus. > > [...] > > You might think that a foreign firm producing in China for sale in China (“in China for China” is a thing) would not register in China’s trade data. After all, goods made in China and sold in China never cross a border, and thus should not show up in the customs data. > > But in the new balance of payments data, China basically reports a trade deficit with itself because of foreign firms producing in China. > > [...] > > If a foreign firm contracts with a Chinese firm to manufacture that foreign firm’s goods in China, and then receives delivery of those goods in China, China counts this as an export. > > [...] > > But the strange turn happens if the foreign firm turns around and sells the good that a contract manufacturer produced for it inside China. Such goods are now being counted as an import in the balance of payments data. > > **Thus, China exports goods to foreign firms operating in China, and then imports those goods back from the same firm even though the goods never leave China. If the goods are sold at a higher price than the contract manufacturer receives, it ends up being reported as a trade deficit in the balance of payments.** > > [...] > > So Chinese production for the Chinese market by foreign firms is somehow generating a trade deficit in the balance of payments data. This, of course, makes no real economic sense. > > [...] > > **Bottom line**: there is no good reason to think that this adjustment in captures anything important about how China’s economy interacts with the global economy. All this “fake” trade deficit does is reduce China’s reported current account surplus—as the goods surplus in the balance of payments is now about $300 billion (over 1.5 percentage points of China’s GDP) smaller than what it should be in the balance of payments data [while the author estimates] the current account surplus to be close to $700 billion even after the drop tied the resumption of tourism in 2023. > > [...] > > What matters for now is that a large number of analysts are using China's current account data to assess China's impact on the world without realizing that the fall in China's surplus since 2021 is basically an artifact of difficult to justify changes in China's balance of payments methodology. The real story is found in the old fashioned goods data.

cross-posted from: https://feddit.org/post/1752069 > [Archived link](https://web.archive.org/web/20240805141452/https://eastasiaforum.org/2024/08/05/rescue-measures-wont-fix-the-structural-problems-in-chinas-property-market/) > > While housing rescue policies may help provide stimulus to property markets, the economic fundamentals currently unfolding in China are unfavourable to their implementation, writes Yixiao Zhou from The Australian National University. > > [...] > > China has one of the world’s highest housing price-to-income ratios at 29.59. China also has a low lending interest rate at around 4 per cent. Considering this, the room for expanding the mortgage scale is limited, constraining the ability of easing lending rules to stimulate housing demand. > > Another short-term demand factor is the transfer of rural homestead land. In June 2024, Nantong, a city in Jiangsu province, introduced new policies that allow individuals who voluntarily relinquish their rural homesteads and buy homes in urban areas to receive financial subsidies. Nantong is not alone in this initiative. Encouraging the voluntary and compensated relocation from rural homesteads has become a key focus of real estate policies. But this does not seem to have affected the decreasing trend of housing prices either. > > [...] > > If downward adjustment in property prices leads to real estate loan default, this will pose major risks to financial stability. Japan’s experience with a massive real estate bubble burst in the early 1990s provides a crucial lesson for policymakers in China. The sharp downturn in the real estate sector led to a prolonged period of economic stagnation known as ‘Japan’s lost decade’. > > [...] > > Ultimately the structural problems holding back demand for properties could be solved by reforms in land allocation, financial market regulation and urbanisation policies. These reforms could help reposition China’s property sector on a healthy and sustainable growth path.

www.euronews.com

www.euronews.com

Local government debt is estimated at up to $11 trillion, including what's owed by local government financing entities that are “off balance sheet,” or not included in official estimates. More than 300 reforms the party has outlined include promises to better monitor and manage local debt, one of the biggest risks in China’s financial system. That will be easier said than done, and experts question how thoroughly the party will follow through on its pledges to improve the tax regime and better balance control of government revenues. “They are not grappling with existing local debt problems, nor the constraints on fiscal capacity,” said Logan Wright of the Rhodium Group, an independent research firm. “Changing central and local revenue sharing and expenditure responsibilities is notable but they have promised this before.” **The scramble to collect long overdue taxes shows the urgency of the problems.** Chinese food and beverage conglomerate VV Food & Beverage reported in June it was hit with an 85 million yuan ($12 million) bill for taxes dating back as far as 30 years ago. Zangge Mining, based in western China, said it got two bills totaling 668 million RMB ($92 million) for taxes dating to 20 years earlier. Local governments have long been squeezed for cash since the central government controls most tax revenue, allotting a limited amount to local governments that pay about 80% of expenditures such as salaries, social services and investments in infrastructure like roads and schools. Pressures have been building as the economy slowed and costs piled up from “zero-COVID” policies during the pandemic.

www.cnn.com

www.cnn.com

> US stocks plunged on Monday morning as Friday’s dismal July jobs report continued stoking fears that the US economy is on shaky legs. > The Dow plunged 1,072 points, or 2.7%. The S&P 500 fell 4.1% and the Nasdaq Composite sank by a whopping 6.3%. > The Cboe Volatility Index, or VIX, which measures bets on expected stock market volatility, surged to 55. The last time the fear gauge hit that level outside of the pandemic was the Great Financial Crisis, in 2008.

Video about job prospects after big tech layoffs Tldr: healthcare, education, transportation, manufacturing is outpacing IT in hiring

www.dw.com

www.dw.com

**As Pakistan works on enacting economic reforms under a multibillion-dollar IMF bailout, Islamabad must first figure out what to do with its mountain of debt owed to China** After cash-strapped Pakistan secured a new $7 billion (€6.5 billion) bailout package from the International Monetary Fund (IMF) in July, Islamabad has started talks with Beijing on reprofiling billions in Chinese debt as it seeks to enact economic reforms. On the table are proposals to delay at least $16 billion in energy sector debt to China, along with extending the term of a $4 billion cash loan facility due to depleting foreign exchange reserves. Last week, Pakistani Finance Minister Muhammad Aurangzeb was in Beijing to present proposals on extending the maturity of debt for nine power plants built by Chinese companies under the multibillion-dollar Pakistan China Economic Corridor (CPEC). On Friday, Prime Minister Shehbaz Sharif told a federal cabinet meeting that he had written a letter to the Chinese government requesting debt reprofiling, Pakistan's Dawn newspaper reported. Reprofiling debt differs from restructuring debt in that the amount is not cut, rather, the due date for repayment is extended. Islamabad is under immense pressure to renegotiate the expensive agreements with power producers, primarily Chinese companies, to bring down electricity prices. Since CPEC was signed in 2015 and became one of largest components of China's Belt and Road Initiative (BRI), Beijing has poured billions of dollars into developing infrastructure in Pakistan. The value of CPEC projects comes in a $65 billion, with the primary goal of building a shipping connection for Chinese goods from Gwadar port on the Arabian Sea over the mountain border into China's Xinjiang region.

www.alternet.org

www.alternet.org

[Archived version](https://web.archive.org/web/20240802223455/https://www.alternet.org/warren-fed-economy/) U.S. Sen. Elizabeth Warren on Friday demanded that the chairman of the Federal Reserve immediately "cancel his summer vacation" and slash interest rates following the release of government data showing weaker-than-expected job growth and an increase in the unemployment rate last month. Warren (D-Mass.), an outspoken critic of the Fed's aggressive interest rate increases, argued in a social media post that Fed Chair Jerome Powell "made a serious mistake not cutting interest rates" at the Federal Open Market Committee's (FOMC) meeting earlier this week. The central bank's policy-setting group opted to hold rates at 5.25% to 5.5% for the 12th consecutive month.

cross-posted from: https://feddit.org/post/1386306 > **Over the past 20 years, China has become the largest lender in the Pacific. Now Tonga, Vanuatu and Samoa are spending some of the biggest sums in the world to repay debts to China, as a proportion of their GDP, according to Lowy Institute analysis.** > > **Pacific countries have some of the highest costs in the world in terms of climate adaptation needs, but these are things that have to be deprioritised to deal with the debt. "It's a trade-off and it's not one that's good," Tonga's finance minister says.** > > Experts say China's EXIM Bank does not forgive foreign debts. "It will ease borrowing terms by extending repayment moratoria or pushing out final loan repayment dates. However, it rarely reduces interest rates," Bradley Parks, executive director of AidData, said. > > - Tonga's annual debt repayments to China are nearly 4 per cent of its GDP — the third-highest level in the world. It's a rate that Lowy research associate Riley Duke calls "astronomically high". > > - AidData analysis has found 85 per cent of China's loan-financed infrastructure projects in Tonga show signs of debt distress. > > - Fiji, Papua New Guinea and Cook Islands also have moderate levels of public debt exposure to China, according to the AidData research lab at William & Mary, a Virginia-based public university in the United States. > > - Vanuatu has struggled less with its debts to China and has met its loan repayments, but a series of economic shocks have set the nation back, including three tropical cyclones in 2023 and the collapse of its national carrier in May. > > - Loan repayments to China commonly drain resources from public services such as health and education, and other pressing needs in the region. In Tonga's case, the government was spending more on servicing its debt than on health.

www.businessdailyafrica.com

www.businessdailyafrica.com

Cross posted from: https://beehaw.org/post/15214106 [Archived version](https://web.archive.org/web/20240724183032/https://www.businessdailyafrica.com/bd/markets/currencies/forex-reserves-fall-sh64bn-on-foreign-debt-repayments-4698862) - Kenya’s foreign exchange reserves have experienced a significant drop of USD 487 million (about KES 63.9 billion) over the past week, following substantial repayments of external debt. - The decrease in reserves follows the government’s repayment of USD 533 million (about KES 70 billion) in external loans, which includes USD 433 million (KES 56.8 billion) used to service a loan from China. - The reduction has decreased the import cover from 4.1 months to 3.9 months. Import cover refers to the number of months the available foreign exchange reserves can finance imports. - Previous reports indicated that Kenya had spent KES 152.69 billion (approximately USD 1.15 billion) repaying China in the last fiscal year This included USD 705.05 million (KES 100.47 billion) in principal repayment and USD 366.46 million (KES 52.22 billion) in interest. - Additionally, Kenya paid USD 286.04 million (KES 40.76 billion) more than initially planned for the fiscal year. - The secretive nature of Beijing’s loan terms with developing countries like Kenya often means borrowers must prioritise repayments to China, placing a considerable burden on the Kenyan public.

www.newsday.co.zw

www.newsday.co.zw

cross-posted from: https://feddit.org/post/1212562 > [Archived link](https://web.archive.org/web/20240725090036/https://www.newsday.co.zw/theindependent/international/article/200030048/belt-and-road-is-code-for-debt-and-distress) > > **In Laos, the tiny Asian country, China became the largest foreign investor with some $5 billion spread across 745 projects, overtaking Thailand. The China-led strategy was meant to protect countries like Laos from economic shocks — instead, it led to them. Today Laos is struggling to repay the billions it borrowed from China to fund the hydroelectric dams, trains and highways, which have drained the country of foreign reserves. As repayments drag, external debt is rising, a vulnerability exacerbated by the pandemic and rising global fuel and food prices.** > > The escalating public debt in Laos has sparked global discussions regarding the sustainability within the region. This concern primarily stems from China’s increasing role as a significant financier of Southeast Asian infrastructure projects, raising fears that China might be using debt to gain geopolitical leverage by ensnaring impoverished nations in unmanageable loan agreements. > > When President Xi Jinping of China proposed the Belt and Road Initiative (BRI) in a pair of speeches in 2013, the initiative became popular in the developing world, where almost all countries face infrastructure deficiencies. Beijing has loaned almost $1 trillion to developing nations in the past two decades. But China was specifically providing debt and burdening borrowing countries with high-interest rates they could not repay. > > [...] > > BRI has also been criticised as an effort to export China’s authoritarian model, as a number of major loan recipients have poor records of democracy and civil liberties like in Cambodia and Laos in Asia. > > What then results is called ‘Debt-trap diplomacy (DTD),’ now associated as a Chinese policy tool connected to BRI. The approach to Debt-trap diplomacy begins by China intentionally lending excessively money to low-income indebted states that cannot later repay Chinese debt. Loan taking nations see a rise in public debt. However, it is difficult to say how much Chinese financing is going to infrastructure in Southeast Asia because the Chinese effort lacks transparency. China’s loans are largely coming from the two policy banks: China Development Bank and China EXIM Bank. They borrow on domestic and international capital markets and lend with a spread, so they expect to be financially self-sufficient.

fortune.com

fortune.com

> In an interview with the Wall Street Journal, the long-time associate of The Black Swan author Nassim Nicholas Taleb said a severe crash is on the way and stocks could lose more than half their value, while acknowledging that his latest warning should come as no surprise. > > “I think we’re on the way to something really, really bad—but of course I’d say that,” Spitznagel said. Since Fortune is mostly citing WSJ, here's an [archive of that WSJ story](https://archive.ph/fNoXB). From that source: > Governments have been so active tamping down any conflagration in the economy that the dry brush of debt and other hidden risks have built into the ingredients for a severe blaze. > >How should mere mortals without access to tail risk hedges respond to his prediction? Probably by doing nothing, says Spitznagel. > >“Cassandras make terrible investors.”

adf-magazine.com

adf-magazine.com

Cross posted from: https://beehaw.org/post/15094770 [Archived version](http://web.archive.org/web/20240718082230/https://adf-magazine.com/2024/07/china-increases-loans-to-africa-while-countries-struggle-with-old-debt/) **Developing countries owe China an estimated $1.1 trillion, and more than 80% of China’s loans are to countries experiencing financial distress, according to AidData, a research lab at William & Mary. Despite this, China rarely agrees to loan forgiveness or principle reduction, preferring to negotiate longer repayment plans on a case-by-case basis.** - Despite promises of two-way trade, African exporters have little access to Chinese markets for their goods. Most of China’s imports from the continent are oil, gas and minerals. - The result is a more one-sided relationship than China says it wants.. One that is dominated by imports of Africa’s raw materials and that some analysts argue contains echoes of colonial-era Europe’s economic relations with the continent. - With the annual Forum on China-Africa Cooperation (FOCAC) set to take place in September, China is expected to announce new projects in Africa. But its lending practices are coming under scrutiny. Several countries that have taken on debt have found themselves forced to make drastic cuts to domestic programs or raise taxes in order to repay the loans. - Kenya, for example, spends about 60% of its revenue on debt payments, with about one-third of that money going to pay the interest on loans.

cross-posted from: https://feddit.org/post/865985 > The fatalistic tag “garbage time” began popping up on social media platforms over the past month. It was given a more recent boost when state media and commentators lined up to denounce the phrase and any suggestion that decline would follow downturn for China. > > “This is a catchphrase insinuating that there’s no help and no hope, denying and downplaying everything in China,” [state-owned media outlet] Beijing Daily said in a commentary last week. > > It follows another buzzword China’s censors have targeted as a threat to stability since it broke into the mainstream three years ago: “lying flat,” a call to a slacker life of limited ambition and quiet protest. > > [...] > > There are other signs China’s collective confidence has suffered, according to survey data collected by Stanford University professor Scott Rozelle and others published in summary last week by the U.S. think tank Center for Strategic and International Studies. > > Rozelle found Chinese respondents to a survey were more pessimistic than they had been two decades ago, more likely to blame structural factors for determining whether a person is rich or poor and far less likely to believe hard work pays off. > > In 2004, 62% agreed “in our country, effort is always rewarded." That dropped to 28% in the 2023 survey.

essanews.com

essanews.com

cross-posted from: https://feddit.org/post/860815 > The Chinese banking sector is facing a severe crisis. In just one week, 40 banks disappeared, and the collapse of Jiangxi Bank has further deepened the sector's problems. > > Cryptocurrency market analyst Sigma G also examined the situation in China's banking sector. He points out that the leading cause of the problems is the deep recession in China's real estate sector. Over-indebted developers and local governments fail to repay loans, leading to financial instability. Property prices have plummeted, and construction projects have been halted, further burdening the economic system. > > The author also highlights the issue of hidden bad debts. Banks have used asset management companies (AMCs) to offload toxic loans, creating an illusion of stability. However, a new banking regulator, the National Financial Regulatory Administration (NAFR), has begun cracking down on these practices by imposing fines and increasing oversight. > > Many Chinese cities and even entire regions are drowning in debt. The liabilities were so high that local government representatives sent envoys to Beijing in the spring. They are negotiating terms for repaying billions in loans. Unpaid debts are increasingly weighing on regional economies, threatening national economic growth.

cross-posted from: https://feddit.org/post/859855 > [Archived version](https://web.archive.org/web/20240717044244/https://meduza.io/en/feature/2024/07/17/watching-your-spending) > > **In 2025, Russia’s Central Bank plans to fully roll out the digital ruble — a new form of currency that, according to officials, can be used on par with cash and electronic payments, and holds the exact same value as the traditional ruble.** > > **The Russian authorities insist that this new tool is safer than cash and that the fees for using it will be lower than for other electronic payment methods. Every digital ruble has its own unique code, which theoretically makes it possible for the Central Bank to restrict its use — and, according to experts from the digital rights group Roskomsvoboda, to monitor citizens’ transactions.** > > - The issuer of this new form of currency is the Central Bank itself, a key difference to conventional bank transfers. Responsibility for its use and management will fall on the state, not on commercial banks. When customers deposit funds into their digital ruble accounts, they will effectively be lending their money to the authorities. > > - At the same time, commercial banks will be responsible for all account operations, as well as for ensuring security. Clients will be able to manage their digital rubles through commercial bank apps. > > - Each digital ruble will always be worth exactly one ruble. However, it’s possible that the authorities will restrict how digital rubles can be spent; the Central Bank may encode certain rubles, for example, so that they can’t be used for gambling or buying alcohol. > > - Unique codes on each digital ruble will allow the government to directly monitor citizens’ spending when they use the new form of currency. > > - The digital ruble could become a major tool in the Central Bank’s management of Russia’s finances, allowing not only the monitoring of transactions (the government already surveils non-cash payments) but also “instantaneous and direct control over monetary policy.” > > - According to the lawyer, the government could use it to instantly implement currency redenomination or impose broad restrictions on money use. “During the COVID restrictions, for example, it would have been possible to use digital rubles to ban payments for [travel] tickets and hotels,” the lawyer said.

www.usatoday.com

www.usatoday.com

I personally would not be interested in buying a new car. They depreciate in value too quickly and do the same exact job as a used car. Used cars also have been run so lemons that come from the factory have been filtered out or fixed.

www.icij.org

www.icij.org

Legal experts say the acquittal of 28 defendants facing Panama Papers-related money laundering charges raises questions about the progress of anti-corruption efforts in Panama and beyond, as the country’s new president welcomed the outcome of the trial and called the original journalistic investigation a “hoax.” In a statement released on Friday, Panama’s judicial branch said the judge Baloisa Marquínez did not find enough evidence to reach a guilty judgment and dismissed a host of electronic evidence presented by prosecutors for not meeting chain-of-custody protocols and authentication standards. Carlos Barsallo, a Panamanian attorney and former president of Transparency International’s Panama chapter, said the decision reflected a blunder by prosecutors since many of those documents were obtained by authorities during an inspection of the offices of Mossack Fonseca, the Panamanian law firm at the center of the Panama Papers leak. Digital documents, like emails, should have made it easy to maintain the chain of custody, Barsallo said. “From a global perspective, it shows the difficulty of these cases and the necessity for the prosecution to have more resources — not just economic, but also human resources and technical know-how,” Barsallo said.

[Archived version](https://web.archive.org/web/20240704164957/https://www.bloomberg.com/news/articles/2024-07-03/china-says-doing-its-best-to-help-tiny-laos-ease-debt-burden) - Communist-run Laos has come to the fore after it opened a high-speed rail line with China in 2021 that cost the landlocked country about $6 billion. While the development is seen by many as the start of a ramp up in infrastructure that directly connects China with Southeast Asia, it has raised concerns of a build-up in debt for Laos and other smaller countries. - China is by far Laos’ biggest creditor, accounting for about half of the $10.5 billion in external government debt. The tiny nation had $13.8 billion in total public and publicly-guaranteed debt at the end of last year, amounting to 108% of its gross domestic product. - Laos’ external debt payments in 2023 reached $950 million, almost double the amount compared to 2022,, making the country defer $670 million in principal and interest payments. The World Bank has said in the past that such moves have provided temporary relief in recent years. - Laos' development is seen by many as a further chapter of China's 'debt-trap diplomacy' as Beijing offers developing countries financial loans under often opaque condition, leaving them grappling with repayments while it supports China’s efforts to expand its economic and political influence in foreign countries. - For example, Sri Lanka fell into default for the first time in its history back in 2022 after its foreign reserves dwindled. Last month the South Asian nation said it reached final restructuring agreements worth $10 billion, including with an Official Creditor Committee of bilateral lenders and China’s Exim Bank. Sri Lanka's port, however, is now owned by China. - China dismissed the “debt-trap diplomacy” allegations.

www.dw.com

www.dw.com

Malaysia and Thailand are the latest nations in Southeast Asia to express interest in joining the expanded BRICS group of emerging economies.

swarajyamag.com

swarajyamag.com

[Archived version](https://web.archive.org/web/20240629020144/https://swarajyamag.com/foreign-affairs/forewarned-by-india-nepal-steps-back-from-chinas-belt-and-road-initiative) - Nepal has shied away from signing a plan to implement China’s ambitious Belt & Road Initiative (BRI) in the Himalayan nation. Resisting immense pressure from Beijing, Nepal’s Prime Minister Pushpa Kamal Dahal refused to greenlight the signing that would have paved the way for the implementation of nine mega and more than a dozen major BRI projects in Nepal. - That’s because soon after Nepal signed the BRI framework agreement in May 2017, India launched a massive but silent campaign to educate and explain Nepal’s political leadership, economists, bureaucrats, diplomats, academia, media and civil society leaders the pitfalls of China’s BRI to them, making Nepal’s top politicians and others fully aware of China’s sinister plan to ensnare nations into a debt trap through the BRI. - PM Deuba eventually told China that Nepal would only agree to a small component of the cost of BRI projects in the form of loans. However, the interest on such loans should not be more than what multilateral lending agencies like the World Bank and Asian Development Bank (ADB) charge for their loans (one per cent per annum). - This was not acceptable to China which charges more than two per cent on the loans it gives to other countries to finance BRI projects. Also, China insists on the contracts for these projects being awarded only to Chinese companies and refuses to do away with or water down penalty clauses (in case of failure to repay the loans on time). **What also worked against China was Nepal’s experience with the Pokhara International Airport which cost US $ 305 million. China’s Exim Bank provided a loan of about US $ 215 million at 2 per cent interest. Chinese firms were awarded contracts for construction and technical works.** **Allegations of shoddy construction, inflated costs and mismanagement by the Chinese have fuelled public anger against China in Nepal. The airport has turned into a huge liability ([read this](https://swarajyamag.com/world/why-india-should-be-concerned-over-chinese-built-airport-at-nepals-pokhara-becoming-a-white-elephant-and-a-chinese-outpost)) since no commercial and scheduled flights are operating from there.**

cross-posted from: https://feddit.org/post/374497 > UniCredit said on Monday it was challenging the terms set by the European Central Bank (ECB) for the Italian bank to cut its exposure to Russia, and seeking a ruling from the European Union's General Court, as well as a freezing of the request in the meantime. > > Euro zone banks still involved with Russia more than two years after Moscow invaded Ukraine have come under growing pressure in recent weeks from the bloc's supervisors, as well as U.S. authorities, over their ties to the country. > > A complex regulatory backdrop, involving Western sanctions against Moscow and local laws in Russia where the Italian group runs a retail bank, meant it had to "seek clarity and certainty" on the actions it needed to take, UniCredit said in a statement two and a half years after Russia's full scale invasion of Ukraine. > > After Austria's Raiffeisen, UniCredit has the biggest exposure to Russia, where it runs a top 15 bank, among European lenders. > > Raiffeisen has no plans to take legal action against the ECB over the request to reduce its Russia-related business, a spokesperson has said. > > "For anyone who believes that Ukraine's fight against Russia is important for the security of Europe, the fact that UniCredit stayed in Russia, made profits, and is now suing the ECB over their attempts to get it to leave, this doesn't look good," said Nicolas Veron of Brussels think tank Bruegel.

After the Federal Reserve disclosed JPMorgan Chase's stress test results 2024, the bank said in a statement that the Fed's projections for a particular asset - the 'Other Comprehensive Income (“OCI”) - was overestimated. "Based on the Firm’s own assessment, the benefit in OCI appears to be too large", the bank says. The meaning of this is that its losses under the exam should actually be higher than the regulator's findings. According to the [Fed's projection (new table opens as pdf)](https://www.federalreserve.gov/publications/files/2024-dfast-results-20240626.pdf), JPMorgan was assigned $13 billion in OCI, more than any of the 31 lenders in this year’s test. It also estimated that the bank would face roughly $107 billion in loan, investment and trading losses in that scenario. Without specifying a number, the bank said that should its analysis be correct, "the resulting stress losses would be modestly higher than those disclosed by the Federal Reserve". Some media reports say the new findings may delay JPMorgan' stock repurchase plans, although the banks did not publicly comment on that. The move is not as unusual as it may seem. In 2023, Citigroup and Bank of America made similar moves and claimed their projected income would differ from the Fed's results. There have also been critics claiming that some aspects of the annual stress test exams were too opaque.

[Archived version](https://web.archive.org/web/20240625053058/https://www.bloomberg.com/news/articles/2024-06-25/china-s-rich-spend-millions-on-shanghai-property-bucking-crisis) - A residence priced $15 million was sold within hours - Buyers snatch 200 large flats priced from nearly $5 million Shanghai’s luxury real estate market is a bright spot in China’s bleak property sector. It’s the only one among the country’s mega cities that’s still attracting people to put down money in an asset class that has otherwise been abandoned. [...] The move is driven by rich Chinese — many dwelling in the Yangtze River Delta region that Shanghai is part of — who are parking their money only in surefire investments [...] buyers are a mixture of locals and outsiders, many from the neighboring Zhejiang and Jiangsu provinces, according to sellers and developer advisers. Shanghai allows non-local homebuyers if they’ve paid income taxes for three years. [...] Shanghai’s more affluent and entrepreneurial demographic is helping with the rebound, whereas the capital has more people working for state-owned enterprises and the government, meaning they already have access to government-subsidized housing. [...] the trend is expected to cool down in the second half, after pent-up demand is released, according an analyst.

fortune.com

fortune.com

**Local governments in China have asked several companies to pay tax bills dating back as far as the 1990s, underscoring their need for funding given the uneven economic recovery and persistent housing slump.** A number of listed firms have said in exchange filings in recent months that they’ve gotten government demands to pay tens of millions in back taxes and warned investors this could impact their earnings. V V Food & Beverage Co. said last week that a liquor-making unit was told to pay some 85 million yuan ($11.7 million) on income it “failed to disclose” for about 15 years starting in 1994. ChinaLin Securities Co., Ningbo Bohui Petrochemical Technology Co., Zangge Mining Co. and PKU HealthCare Corp. have issued similar statements. China’s local governments are facing unprecedented pressure to expand revenues because economic growth is slowing and the contracting real estate market has sent income from land sales plunging. Their already elevated debt stockpile is limiting their ability to leverage up further, forcing the central government to borrow more and give them the funds. The tax recovery is “likely due to the fiscal distress of local governments,” said Xing Zhaopeng, an analyst at Australia & New Zealand Banking Group. “I think they need some money to pay by quarter end” because regional authorities usually pay contractors of government projects then, he added. Local governments booked less than 5.8 trillion yuan in revenues under the general public budget and the government-fund account, which include taxes and land sales income, in the first four months of the year. That figure was less than the more than 5.9 trillion yuan in the same period last year, according to data from the Finance Ministry. Their spending also fell to just under 10 trillion yuan from 10.4 trillion yuan a year earlier.

**China’s economy is buried under a great wall of debt and Xi Jinping’s answer is to add more bricks. The president has sanctioned an extraordinary programme of borrowing by the central government to steer the $18 trillion behemoth to “high quality development”. In doing so, he is piling risk onto the country’s last decent balance sheet.** There is nothing new in the Chinese central government taking on more debt in a time of crisis. But the latest plan, outlined in March by the State Council, to sell special sovereign bonds with maturities of up to 50 years is a departure from a tested formula. Such debts used to be indeed special, with only three new issuances by the People’s Republic before last month. All had a one-off policy goal or specific emergency to deal with, such as bailing out insolvent state-owned banks in 1998. This time, the government will sell 1 trillion yuan ($138 billion) in ultra-long-dated, special sovereign bonds. These issues will continue over “each of the next several years”, and the policy goals are broad. Much of the proceeds will be used for investment to support “major national strategies”, per the State Council. Beijing would help finance the construction cost of schools and hospitals in grain-producing counties, for instance, to reinforce food security and thereby China’s self-sufficiency. Additionally, new industries such as semiconductors, electric vehicles and artificial intelligence will be prioritised as China races to establish a growth model led by domestic consumption, a green economy and innovation, rather than one that depends on infrastructure, land and labour. Taking on more borrowing at the central government also will consolidate Xi’s grip on economic planning and resource allocation, potentially helping China to reduce wasteful investments. Crucially, expanding the central government’s balance sheet will ease the future burden on cash-strapped local governments that are responsible for most spending. **Heavy lifting** Xi’s borrowing plan addresses a problem created by a tax-sharing system introduced in the 1990s which allows Beijing to take a lion’s share of the national tax revenues. By 2022, per Ministry of Finance data, local governments were responsible for nearly 90% of total government expenditure but they needed to make do with about 50% of total government revenue. The squeeze gave rise to local government financing vehicles, known as LGFVs, and prompted municipalities to lean on property market income including land sales to balance their books. Property incomes accounted for more than 40% of local government income in 2020. It dwindled quickly thereafter due to Xi’s “three red lines”, a deleveraging campaign that ultimately led a Hong Kong court to order the liquidation of Evergrande, the world’s most indebted real estate developer. **Borrowing binge** The additional borrowing is riskier this time. In 1998 China was on the verge of joining the World Trade Organization. Powered by robust exports and a youthful workforce, its trajectory was firmly on the up. Geopolitical tension, however, has taken steam out of the world’s second largest economy. Its sheer size and its existing indebtedness are an issue too. The central government’s balance sheet remains tidy for now. Its outstanding borrowings amounted to 24% of GDP at the end of 2023, the International Monetary Fund estimates, among the lowest of major economies. If all else remains equal and China issues special sovereign bonds to the tune of 1 trillion yuan each year for the next decade, its borrowings would rise nearly 8 percentage points to almost 32% of last year’s GDP, Breakingviews calculates. The problems stack up elsewhere, however. Explicit local government debt amounted to another 31% of GDP by the end of 2023, per the IMF, LGFVs account for a further 48%, and other government funds another 13%, bringing the augmented debt up to 116 trillion yuan, about $16 trillion, or 116% of GDP – a 35% increase on 2018, the IMF calculates. Corporate debt adds another 123% of GDP, much of it issued by state banks and owed by state-owned enterprises, plus there’s household debt at 61% of GDP, per Fidelity which calculates gross debt at over 300% of GDP. Borrowing more doesn’t sound like “a basket of comprehensive measures” to resolve risks stemming from local government debts, as the ruling Communist Party’s Politburo called for last year. The potential costs of bailing out those authorities and making the shift to the new growth model is why Moody’s and Fitch, two of the three major rating agencies, have put China’s sovereign rating on negative outlook since December. More than two decades ago Zhu Rongji reacted indignantly to Hong Kong newspapers’ assessment that he was China’s “deficit premier” when his government started selling long-term construction bonds at smaller amounts. He insisted his cabinet was investing in quality assets, for future generations of the People’s Republic. This gamble paid off and the projects, including a power grid and an extensive mobile telecommunication network, laid the foundation for decades of growth. By the time the new wave of sovereign debt matures, the People’s Republic would be celebrating its 100th anniversary and, if all goes well according to Xi’s plan, it will be a “strong and modern socialist country”. Long before then, however, it will be clear whether China can defy a debt crisis, as it has done so for decades, and simultaneously revive growth. There will be even less room to borrow its way out of problems next time.

[Archived link](https://web.archive.org/web/20240614181315/https://meduza.io/en/feature/2024/06/14/we-have-no-choice-now) **For over half a year, Russian companies have been facing difficulties in processing payments with China. Fearing secondary sanctions, banks are refusing to transfer funds, leaving importers unable to bring goods into the country. Vladimir Putin raised this issue during his visit to Beijing in May, but the situation doesn’t seem to have improved.** On December 22, 2023, U.S. President Joe Biden signed an executive order allowing sanctions to be imposed on banks from third countries if they are caught aiding the Russian military-industrial complex. Once blacklisted, these companies would be banned from holding correspondent accounts in American banks, meaning they’d be unable to conduct any dollar transactions. Following this order, dozens of Chinese financial organizations refused to accept transfers from Russia — not only in U.S. dollars but also in Chinese yuan. On June 12 of this year, Washington tightened its demands. Previously, transactions involving five sectors of the Russian economy — technology, defense, construction, aerospace, and manufacturing — were under scrutiny. Now, the U.S. Treasury has expanded the definition of the military-industrial complex to include all companies previously sanctioned under Executive Order No. 14024. This means that the number of Russian entities that foreign banks must avoid to maintain access to dollar transactions has significantly increased. According to Castellum.AI, there are more than 4,000 such organizations. Biden’s executive order — neither in its new nor old versions — has yet to be enforced against banks from third countries. So far, representatives of the U.S. administration have only issued verbal warnings: Secretary of State Antony Blinken expressed “serious concern” about the supply of machines and microelectronics to Russia, and Treasury Secretary Janet Yellen publicly mentioned the sanctions risk during her visit to China in early April. This was enough to trigger significant shifts in trade between Russia and China. By the end of 2023, trade turnover had increased by 26 percent to a record $240 billion. However, in April 2024, China’s customs authority reported a 15 percent reduction in deliveries of cars, equipment, and other machinery. Bloomberg noted that exports to Russia fell for the first time in two years, linking this to sanctions risks. Chinese exports to Russia also fell in May, and Russian customs confirmed the continued decline of imports from Asia. Russia’s Central Bank acknowledged that it had become generally more difficult for Russian banks to open correspondent accounts abroad, even in “friendly” currencies, and directly linked this to “sanctions the United States adopted in December 2023.” The issue was also discussed at the St. Petersburg International Economic Forum. Industry players reported that money transfers from Russia to China could take as long as three months, and even then might end up being returned to the sender. Businesses complained that they couldn’t even pay for theater decorations or children’s displays. Pavel Brun, the head of MasterProf, said his company hasn’t been able to arrange the supply of plumbing fixtures. “It’s like walking through a minefield,” he told Business FM. **Finding a workaround** Some hopes were pinned on Vladimir Putin’s mid-May visit to China. However, although Putin mentioned that the payment issue was discussed, he didn’t provide any specifics, and business owners confirmed that the difficulties in making payments persisted even after the delegation returned to Moscow. A source in the trade industry told Reuters that the typical way Russian businessmen solve this problem is by going “from bank to bank, opening current accounts.” “If their payment doesn’t go through, they go to the next one,” the source explained. In response, Chinese financial institutions have started imposing additional requirements, such as asking for an office lease agreement in the province where the bank is located. “While this would have seemed like a harsh requirement before, we have no choice now,” business owners commented to Kommersant FM. One of the most promising options was to open an account at the Chinese branch of the Russian bank VTB. The demand for this was so high that businesses were often left waiting as long as a year to open an account. VTB Bank CEO Andrey Kostin promised to more than double the staff to speed up this service. However, in its broadened interpretation of Russia’s military-industrial complex, the U.S. Treasury directly named VTB as one of the banned entities for transactions. This will likely complicate the bank’s operations. As an alternative, businesses have started using banks in third countries as intermediaries, sending money through companies in Hong Kong, Kazakhstan, Kyrgyzstan, the U.A.E., and other “friendly” jurisdictions, rather than directly from Russia, according to Reuters sources. This scheme can prove costly: intermediaries may charge a commission of several thousand dollars per transaction, they don’t guarantee success, and the sender will have trouble getting the money back if the payment fails. Goods may also be confiscated in the intermediary countries. Nevertheless, half of the payments are currently processed this way. Some companies have started using cryptocurrency to make payments to China, specifically the stablecoin Tether, which is pegged to the U.S. dollar, reports Bloomberg. Instead of waiting months, payments are processed in 5-15 seconds, and without the hefty commissions intermediaries charge. However, there are risks for Chinese partners: since 2021, the local regulator has deemed all cryptocurrency transactions illegal. To circumvent these issues, an even more unorthodox solution has been devised: Russian steel companies are now bartering metal for any goods that Chinese businesses are willing to offer. This way, no cross-border financial transactions are needed at all. Both Russian customs and the Industry and Trade Ministry have noted the growing popularity of this bartering system. If businesses still need to make monetary payments, they often turn to small rural banks in northeastern China. According to Reuters, these banks, located along the Russian border, are willing to accept transfers and have less stringent compliance requirements. However, due to high demand, even these banks have waiting lists to open an account that stretch for several months. The System for Transfer of Financial Messages (SPFS) — Russia’s SWIFT analogue for domestic and international transactions — could potentially help. However, VTB has complained that too few foreign companies are currently connected to it. Additionally, the system was developed by the Central Bank, which deters non-residents from using it due to sanctions risks. And with good reason: Bloomberg pointed out that the E.U. and the G7 could jointly impose sanctions for connecting to the system. **Ripple effects** Paradoxically, the current payment issues are having a positive impact on the Russian economy. The inability to transfer money has hit imports, thereby reducing the demand for foreign currency. This supports the ruble exchange rate, as noted in the Central Bank in official reports. The bank doesn’t believe this factor will have a significant impact on GDP. However, as Sofia Donets, the chief economist at Tinkoff Investments, told RBC, these problems will ultimately lead to additional costs for sellers. The Moscow-based investment company Tsifra Broker concurs that prices for many goods could rise if timely shipments can’t be ensured. Categories making up the largest share of Chinese exports to Russia are at risk: equipment, land transport vehicles, electrical machinery, and electrical equipment. Currently, importers are complaining that fraudsters are trying to exploit the situation: they write to Russian entrepreneurs posing as Chinese partners and notify them of a change in banking details. There’s been at least one known case where a business ended up sending money to an account, only to find that they couldn’t reach the sender afterward and were left without the paid-for goods. Some market participants believe that resolving the payment crisis will depend on how much banks can earn from conducting such operations. For instance, Anatoly Semenov, director of the Parallel Import Association, points out that so long as the markets of countries unfriendly to Russia are of interest to Chinese businesses, they won’t openly violate the sanctions regime and risk their investments. Banks in Turkey and the U.A.E. are also refusing transactions with Russia. Against this backdrop, The Bell estimates that imports from some countries have dropped by a third this year.